Bass-Financial Mathematics2003-Lecture Notes Series

The Paris-Princeton Lectures in Financial Mathematics, of which this is the second volume, will, on an annual basis, publish cutting-edge research in self-contained, expository articles from outstanding – established or pcoming! – specialists. The aim is to produce a series of articles that can serve as an introductory reference for research in the field. It […]

(Lecture Notes Series)")

The Paris-Princeton Lectures in Financial Mathematics, of which this is the second volume, will, on an annual basis, publish cutting-edge research in self-contained, expository articles from outstanding - established or pcoming! - specialists. The aim is to produce a series of articles that can serve as an introductory reference for research in the field. It arises as a result of frequent exchanges between the finance and financial mathematics groups in Paris and Princeton. This volume presents the following articles: "Hedging of Defaultable Claims" by T. Bielecki, M. Jeanblanc, and M. Rutkowski; "On the Geometry of Interest Rate Models" by T. Björk; "Heterogeneous Beliefs, Speculation and Trading in Financial Markets" by J.A. Scheinkman, and W. Xiong.

برچسبها :

مقالات مرتبط

How Large Is Liquidity Risk In An Automated

Liquidity Risk We introduce a new empirical methodology that takes account of \liquidity risk in a Value-at-Risk framework, and quantify \liquidity risk premiums for portfolios a n d individual stocks traded on the automated auction market Xetra which operates at various European exchange s. When constructing liquidity risk measures we allow for the potential price […]

Mcgraw-Hill, The Triumph Of Contrarian Investing – Crowds, Manias, And Beating The Market By Goin

Contrarian investing what it is, how it works, and why millions of successful investors see it as the only logical choice”(Davis is) one of the most widely respected technical market analysts operating today.” Louis Rukeyser. Contrarians say that, when it comes to investing, the crowd is wrong more often than it is right and prove […]

Traders trick Entry

Traders trick The prerequisite for this material is having studied “The Law of Charts.” Study it thoroughly. You must know about 1-2-3 formations, Ledges, Consolidations, and Ross hooks. In this presentation, we review and go into great depth concerning the Traders Trick Entry (TTE). The TTE is one of the most important concepts you will […]

آخرین مقالات

FT ADX Color Candles اندیکاتور MT5

معرفی و دانلود اندیکاتور کاربردی FT ADX Color Candles اندیکاتور کاربردی FT ADX Color Candles زمانی که نیاز دارید به طور همزمان به چندین مورد نگاه کنید، معامله می تواند بسیار خسته کننده باشد. اندیکاتور کاربردی FT ADX Color Candles قالب شمع ها، ساپورت ها، مقاومت ها، برنامه ها، اخبار و اندیکاتورها. هدف این ابزار […]

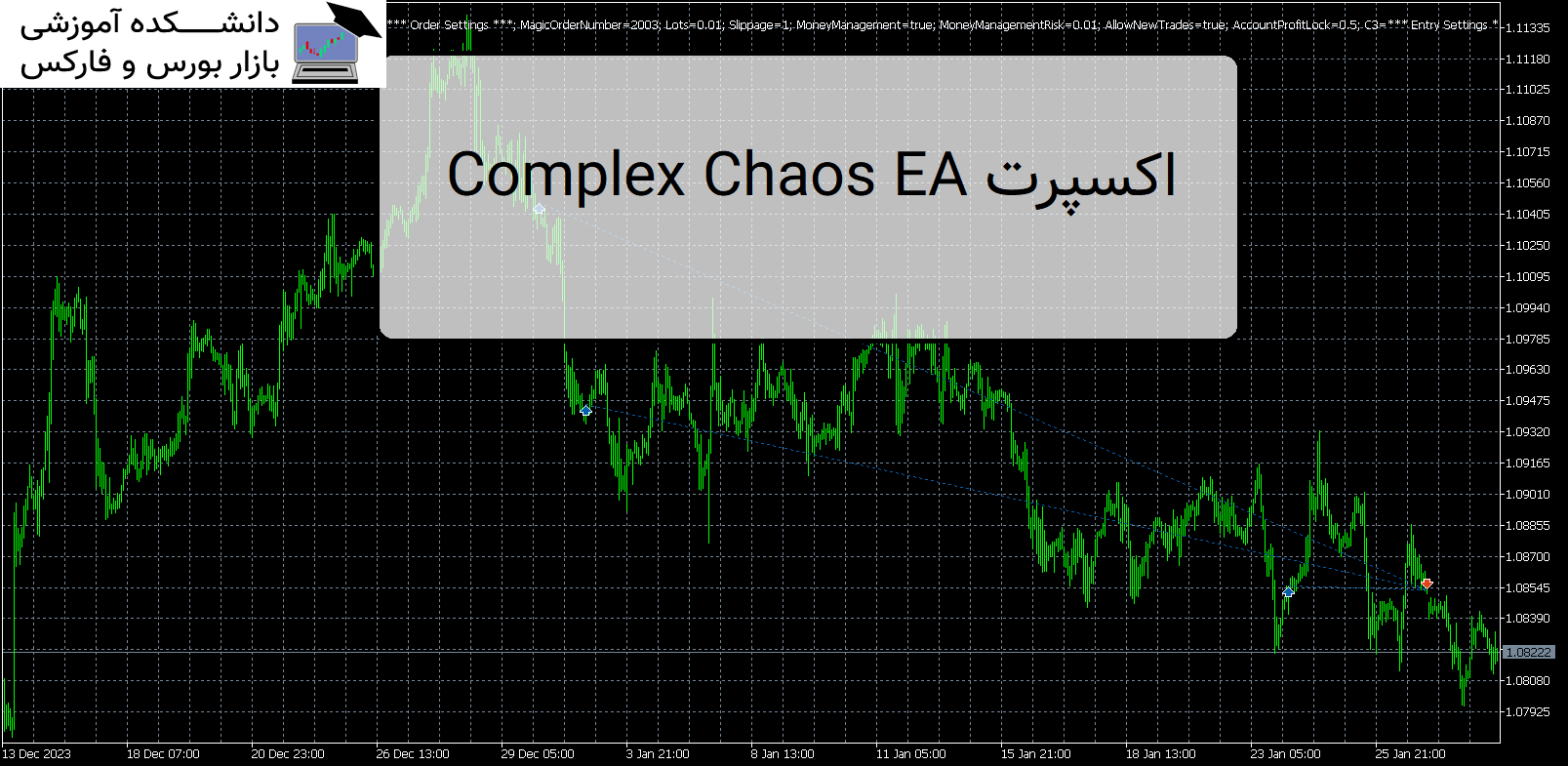

Complex Chaos EA اکسپرت MT5

معرفی و دانلود اکسپرت کاربردی Complex Chaos EA Complex Chaos EA یک سیستم خودکار است که از یک جفت میانگین متحرک نمایی برای تشخیص جهت بازار استفاده می کند و معاملات را در حالت شمع باز باز می کند. معرفی اکسپرت کاربردی Complex Chaos EA اگر بازار بر خلاف یک معامله حرکت کند، در یک […]

Terraforming 1 اکسپرت MT5

معرفی و دانلود اکسپرت کاربردی Terraforming اولین نسخه من از اکسپرت کاربردی Terraforming 1 . EA از آربیتراژ آماری برای کسب سود از جفت ارز USD EUR و GBP استفاده می کند. معرفی اکسپرت Terraforming 1 موقعیت ها زمانی باز می شوند که یک فرصت آربیتراژ شناسایی شود. پوزیشن ها پس از 3 ساعت یا […]

-

فایل های که پسوند آنها rar یا zip یا 7z هست را چگونه باز کنم؟

توسط نرم افزار Winrar فایل را از حالت فشرده خارج کنید و بعد برای اجرا و یا نصب اقدام کنید. دانلود WINRAR

فایل های با فرمت mq4 و mq5 را چگونه اجرا کنم ؟جهت اجرای این نوع فایل ها برای نسخه mq4 باید متاتریدر 4 را روی سیستم خود و برای نسخه mq5 متاتریدر 5 را روی سیستم عامل خود نصب داشته باشید . جهت راهنمایی کلیک کنید

-

رمز تمامی فایل ها :

- عنوان مقاله : ...Bass-Financial Mathematics2003-Lecture

- نوع فایل : PDF

- حجم فایل : 340 کیلوبایت