برچسب: Stock Exchange

5 / 0

De Matos And Fernandes-Testing The Markov Property With Ultra-High Frequency Financial Data

This paper develops a framework to nonparametrically test whether discretevalued irregularly-spaced financial transactions data follow a Markov process. For that purpose, we consider a specific optional sampling in which a continuous-time Markov process is observed only when it crosses some discrete level. This framework is convenient for it accommodates not only the irregular spacing of […]

برچسب: Stock Exchange

5 / 0

Bessembinder And Venkataraman-Does An Electronic Stock Exchange Need An Upstairs Market

We examine block trades on the Paris Bourse to test several theoretical predictions regarding upstairs trading, and exploit cross-sectional variation in “crossing rules” on the Paris Bourse to provide evidence on their relevance. Paris provides an excellent setting to test the implications of upstairs intermediation models, because its electronic limit order market closely resembles […]

برچسب: Stock Exchange

5 / 0

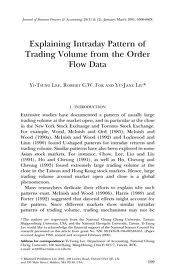

Lee, Fok And Liu – Explaining Intraday Pattern Of Trading Volume From The Order Flow Data

Trading Volume Extensive studies have documented a pattern of usually large trading volume at the market open, and in particular at the close in the New York Stock Exchange and Toronto Stock Exchange. For example, Wood, McInish and Ord (1985), McInish and Wood (1990a), McInish and Wood (1992) and Lockwood and Linn (1990) found U-shaped […]

برچسب: Stock Exchange

5 / 0

Exchange Rules For The Frankfurt Stock Exchange

Stock Exchange For the admission of shares a distinction is made between General Standard,the segment with the statutory minimum requirements of the Regulated Market, and Prime Standard, a segment with additional, international transparency standards. Admission to trading on the regulated unofficial market leads to the Open Market with its Entry Standard segment. Stock Exchange

برچسب: Stock Exchange

5 / 0

Hollifield, Miller, Sandas And Slive-Liquidity Supply And Demand In Limit Order Markets

Liquidity Supply and Demand in Limit Order Markets* We model a trader’s decision to supply liquidity by submitting limit orders or demand liquidity by submitting market orders in a limit order market. The bestquotes and the execution probabilities and picking-off risks of limit orders determine the price of immediacy. The price of immediacy and the […]

برچسب: Stock Exchange

5 / 0

Market Making and Reversal on the Stock Exchange

Market Making and Reversal on the Stock Exchange The accurate record of stock market ticker prices displays striking properties of dependence. We find for example that after a decline of 1/8 of a point between transactions, an advance on the next transaction is three times as likely as a decline. Further examinations disclose that after […]

برچسب: Stock Exchange

5 / 0

Patterns In Three Centuries Of Stock Market Prices

Stock Market Prices This article applies autoregression and rescaled range statistics to very long stock market series to test the hypothesis that long-term temporal dependencies are present in financial data. For the annual capital appreciation returns to the London Stock Exchange, evidence of persistence in raw returns greater than five years and of mean reversion […]

برچسب: Stock Exchange

5 / 0

the nyse tick index and candlesticks

Awealth of information waits to be discovered in the New York Stock Exchange (NYSE) tick index. Its strong suit is its simple calculation. At any point, this index represents the number of stocks trading on an uptick minus the number of stocks trading on a downtick. Extreme tick readings of greater than +600 may indicate […]

برچسب: Stock Exchange

5 / 0

Tick

Indicators such as the TICK can reveal the internal strength (or weakness) of the market and highlight intraday turning points.H e r e ’s how one trader combines the TICK with support and resistance tahlil and retracement levels. The TICK is a market breadth indicator that measures the d i ff e rence between the […]