Hartmann, Manna And Manzanares-The Microstructure Of The Euro Money Market

This paper provides an empirical examination of the microstructure of the euro money market, especially the overnight market, the interbank market for short-term funds in the transnational currency created in January 1999. The institutional framework shaping the microstructure of the money market can be delimited as the union of: central banks’ interest-setting bodies and their […]

This paper provides an empirical examination of the microstructure of the euro money market, especially the overnight market, the interbank market for short-term funds in the transnational currency created in January 1999. The institutional framework shaping the microstructure of the money market can be delimited as the union of: central banks’ interest-setting bodies and their long-term policy strategy;instruments for monetary policy operations and liquidity management;the private market financial instruments and trading mechanismsfor funds; and, (4) the payment and settlement infrastructure for the transfer of those funds.All four elements can significantly influence the intraday behaviour of money market rates.To study their effects on the euro money market, 5 months of intraday data for overnight deposits have been recorded from brokers in four euro area countries and the UK (posting their quotes on Reuters) and from the Italian electronic market MID. The results show “twohump”shaped (or “u”-shaped) intraday patterns of quoting frequency and volatility, but flatterintraday patterns (sometimes weakly single hump”-shaped) for bid-ask spreads. E

ven intraday overnight rate levels hardly differ across brokers located in different euro area countries,reflecting the high integration of this market already shortly after the introduction of the euro,despite some remaining heterogeneities in market structures and trading channels. Quoting activity, rate volatility and spreads increase on ECB Governing Council days, particularly afterthe 1.45 pm release time of interest rate decisions. However, since the amplitude of this volatilityis economically small and since turnovers are not indicative of adverse selection, the average degree of policy uncertainty seems to have been rather limited during our sample period. ECB announcements of new M3 data, related to the first pillar of its monetary policy strategy, around 10am seem to be associated with very moderate increases in short-term volatility.Tuesdays’ Eurosystem main refinancing auctions with the open market exhibit active pre- and post-auction liquidity re-allocation, but only a very short and moderate increase in volatility after the announcement of the allotments and no signs of market power or adverseselection. Open market operation settlement days exhibit the highest turnovers during the busi-ness week, at least for the MID, without, however, being affected by any special risks. Finally,it is shown that spreads and volatility tend to be very high at the end of the minimum reservemaintenance period and that the same happened during the year 2000 changeover days,reflecting the high risks involved in both. 2001 Elsevier Science Ltd. All rights reserved.

برچسبها :

مقالات مرتبط

Asset Pricing with Speculative Trading

Speculative trading stems from disagreements among traders. Besides the approaches based on the existence of private information (and noise traders) or the di erences of opinions, Harrison and Kreps(1978) and Morris(1996) relied on the presence of diverse beliefs to explain speculative phenomena. This paper proposes a new model of speculative trading by introducing rational beliefs of […]

Barclay And Hendershott-Price Discovery And Trading After Hours

We examine the effects of trading after hours on the amount and timing of price discovery over the 24-hour day. A high volume of liquidity trade facilitates price discovery.

Ito And Hashimoto-High-Frequency Contagion Of Currency Crises In Asia

Currency Crises Using daily data for the period of Asian \Currency Crises, this paper examines high – frequency contagious effects among Asian six countries. In this paper, w e distinguishes “origin” (o f exchange rate depreciation, o r decline in stock prices) and “affected” (currencies, o r stock prices) in a sense that the origin […]

آخرین مقالات

FT ADX Color Candles اندیکاتور MT5

معرفی و دانلود اندیکاتور کاربردی FT ADX Color Candles اندیکاتور کاربردی FT ADX Color Candles زمانی که نیاز دارید به طور همزمان به چندین مورد نگاه کنید، معامله می تواند بسیار خسته کننده باشد. اندیکاتور کاربردی FT ADX Color Candles قالب شمع ها، ساپورت ها، مقاومت ها، برنامه ها، اخبار و اندیکاتورها. هدف این ابزار […]

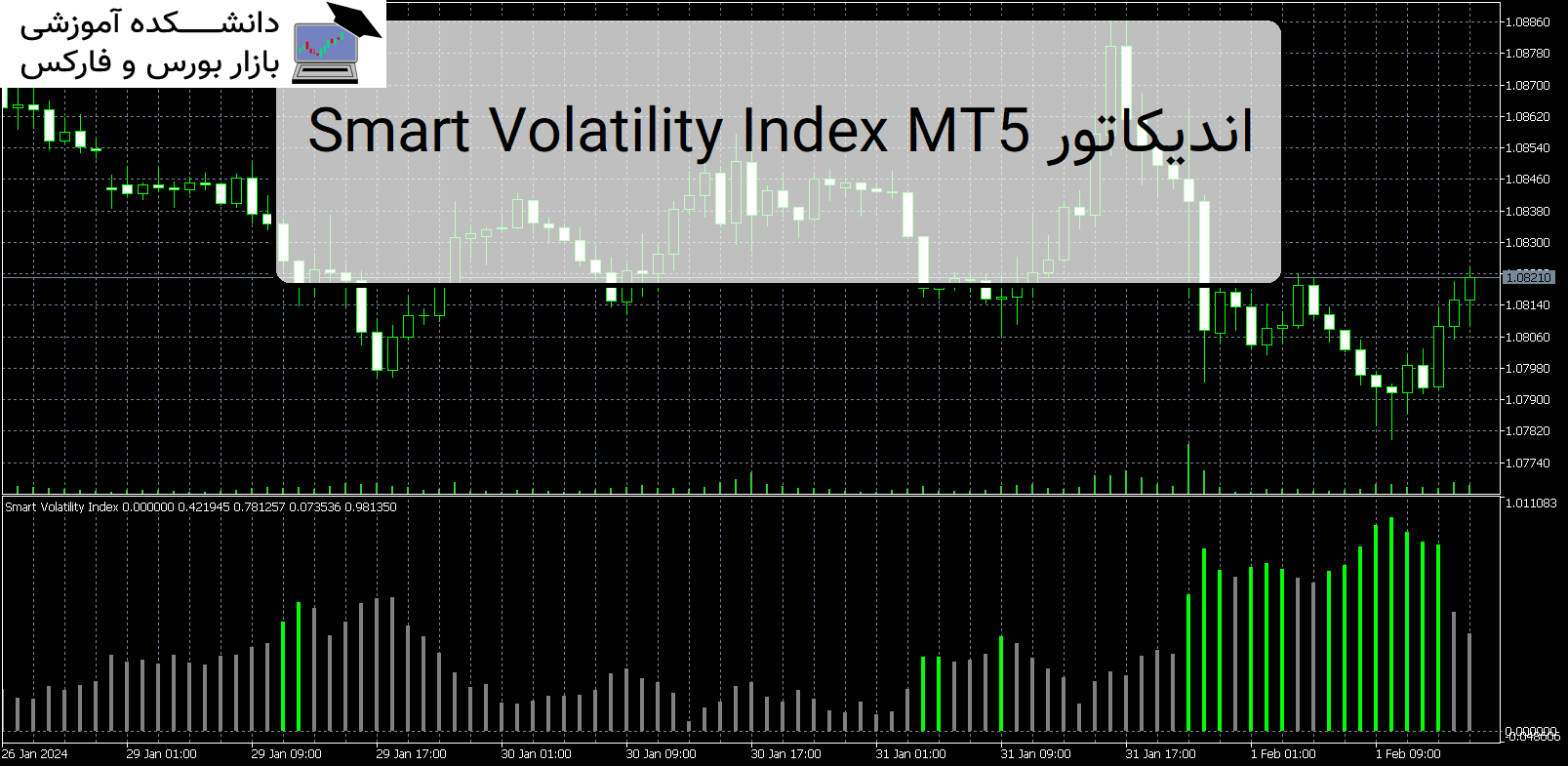

Smart Volatility Index MT5 اندیکاتور

معرفی و دانلود اندیکاتور کاربردی Smart Volatility Index MT5 Smart Volatility Index MT5 از محبوب ترین و با رتبه بندی بالای شاخص نوسانات (VIX) در بازار است. این خوانش همان چیزی است که VIX برای شاخص های سهام انجام می دهد. معرفی اندیکاتور کاربردی Smart Volatility Index MT5 با این حال، این شاخص در تمام […]

Renkochart and Supertrend اندیکاتور MT5

معرفی و دانلود اندیکاتور کاربردی Renkochart and Supertrend Renkochart and Supertrend شاخص فوق روند را در زمان واقعی نمایش می دهد. پس از نصب اندیکاتور، پنجره نمودار Renko و نشانگر supertrend را در همان پنجره نمایش می دهد. معرفی اندیکاتور کاربردی Renkochart and Supertrend این به شما این امکان را میدهد که نقاط ورودی و […]

-

فایل های که پسوند آنها rar یا zip یا 7z هست را چگونه باز کنم؟

توسط نرم افزار Winrar فایل را از حالت فشرده خارج کنید و بعد برای اجرا و یا نصب اقدام کنید. دانلود WINRAR

فایل های با فرمت mq4 و mq5 را چگونه اجرا کنم ؟جهت اجرای این نوع فایل ها برای نسخه mq4 باید متاتریدر 4 را روی سیستم خود و برای نسخه mq5 متاتریدر 5 را روی سیستم عامل خود نصب داشته باشید . جهت راهنمایی کلیک کنید

-

رمز تمامی فایل ها :

- عنوان مقاله : ...Hartmann, Manna And Manzanares-The

- نوع فایل : PDF

- حجم فایل : 470 کیلوبایت