Kalman Filter For Arbitrage Identification In High Frequency Data

We present a methodology for modelling real world high frequency financial data.The methodology copes with the erratic arrival of data and is robust to additive outliers in the data set. Arbitrage pricing relationships are formulated into a linear state space representation. Arbitrage opportunities violate these pricing relationships and are analogous to multivariate additive outliers. Robust […]

We present a methodology for modelling real world high frequency financial data.The methodology copes with the erratic arrival of data and is robust to additive outliers in the data set. Arbitrage pricing relationships are formulated into a linear state space representation.

Arbitrage opportunities violate these pricing relationships and are analogous to multivariate additive outliers. Robust identification/filtering of arbitrage opportunities in the data is accomplished by Kalman filtering.

The state space model used to describe the pricing relationships is general enough to handle both linear and non-linear models. The recursive Kalman equations are adapted to filter tick data, cope with the erratic arrival of observations and produce estimates of all the arbitrage prices on every time step.

We demonstrate the methodology with a robust neural network filter applied to foreign exchange triangular arbitrage. Tick data from three markets is used: $/DM,£/$, £/DM 1993-1995. The filter produces estimates of the arbitrage price for all exchange rates on every second, increasing both the speed and efficiency of arbitrage identification.

File Size: 188KB File Type: PDF Pages: 20

برچسبها :

مقالات مرتبط

Liquidity in Forex Markets

The forward foreign exchange market is modelled within the framework of a limited participation two-country model and then simulated using the artificial economy methodology.The new model improves on the standard two-country cash-in-advance model in a number of ways. It gets closer to the observed lack of autocorrelation in spot returns and it helps to explain […]

Engle And Lange-Predicting Vnet – A Model Of The Dynamics Of Market Depth

The paper proposes a new intraday measure of market liquidity, VNET, which directly measures the depth of the market corresponding to a particular price deterioration. VNET is constructed from the excess volume of buys or sells associated with a price movement. As this measure varies over time, it can be forecast and explained. Using NYSE […]

Kenneth.R.Trester – 101 Option Trading Secrets

Kenneth.R.Trester – 101 Option Trading Secrets Introducing Ken Trester’s book-101 Option Trading Secrets Author of the best-selling Complete Option Player, now in its 4th edition, Ken Trester is acclaimed for rendering complex subjects into easy-to-understand concepts and ideas.

آخرین مقالات

FT ADX Color Candles اندیکاتور MT5

معرفی و دانلود اندیکاتور کاربردی FT ADX Color Candles اندیکاتور کاربردی FT ADX Color Candles زمانی که نیاز دارید به طور همزمان به چندین مورد نگاه کنید، معامله می تواند بسیار خسته کننده باشد. اندیکاتور کاربردی FT ADX Color Candles قالب شمع ها، ساپورت ها، مقاومت ها، برنامه ها، اخبار و اندیکاتورها. هدف این ابزار […]

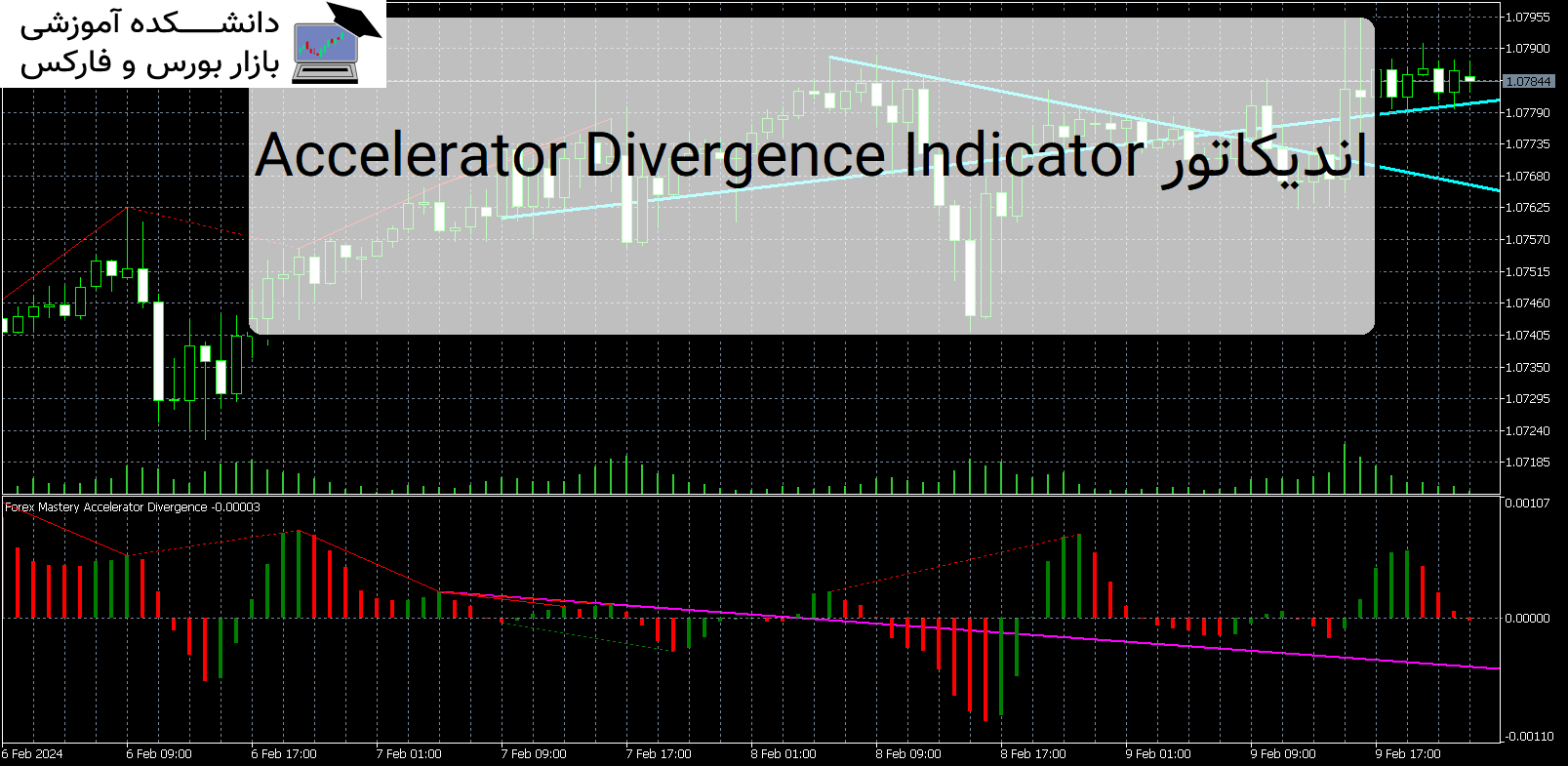

Accelerator Divergence Indicator اندیکاتور MT5

دانلود و معرفی اندیکاتور کاربردی Accelerator Divergence Indicator معرفی اندیکاتور کاربردی Accelerator Divergence Indicator ، ابزاری قدرتمند که برای ارتقای تجربه تجارت فارکس شما طراحی شده است. معرفی اندیکاتور Accelerator Divergence Indicator این شاخص نوآورانه به طور خاص برای شناسایی واگرایی بازار ساخته شده است و به معامله گران بینش ارزشمندی برای تصمیم گیری آگاهانه […]

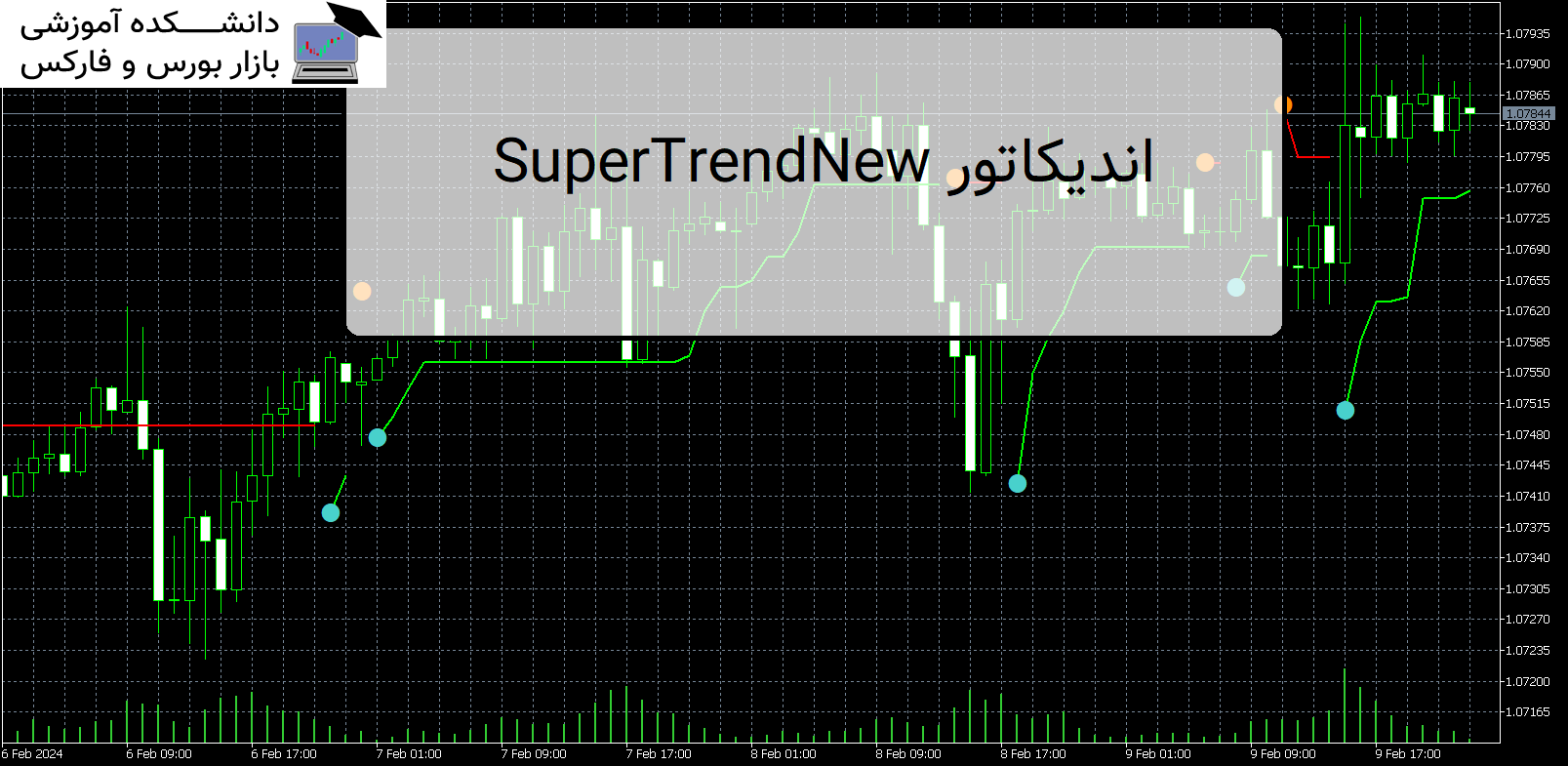

SuperTrendNew اندیکاتور MT5

معرفی و دانلود اندیکاتور SuperTrendNew SuperTrendNew به شما این امکان را می دهد که از تغییر روند سوپرترند، طولانی یا کوتاه را وارد کنید. هر دو دوره ATR و ضرب کننده ATR قابل تنظیم هستند. معرفی اندیکاتور SuperTrendNew اگر «تغییر روش محاسبه ATR» را علامت بزنید، محاسبه بر اساس SMA انجام میشود و نتایج کمی […]

-

فایل های که پسوند آنها rar یا zip یا 7z هست را چگونه باز کنم؟

توسط نرم افزار Winrar فایل را از حالت فشرده خارج کنید و بعد برای اجرا و یا نصب اقدام کنید. دانلود WINRAR

فایل های با فرمت mq4 و mq5 را چگونه اجرا کنم ؟جهت اجرای این نوع فایل ها برای نسخه mq4 باید متاتریدر 4 را روی سیستم خود و برای نسخه mq5 متاتریدر 5 را روی سیستم عامل خود نصب داشته باشید . جهت راهنمایی کلیک کنید

-

رمز تمامی فایل ها :

- عنوان مقاله : ...Kalman Filter For Arbitrage Identification

- نوع فایل : PDF

- حجم فایل : 187 کیلوبایت